The world built on one molecule is changing shape

A HEC Alumni masterclass on the geopolitics of energy laid bare a fracture that no policy, no summit, and no clean-tech roadmap has yet resolved.

On the evening of June 10th, as oil markets absorbed the latest dispatches from the Strait of Hormuz, a room of executives, investors, and alumni gathered at the Maison des HEC in Paris to hear Jean-Michel Gauthier — Professor at HEC Paris, specialist in Energy and Finance, with over thirty years at the heart of the global energy industry — make sense of a world that has stopped making easy sense.

What followed was not a reassuring presentation. It was something rarer and more valuable: an honest map of where we are, where we are going, and why the gap between the two is larger — and more dangerous — than most people in power are willing to admit.

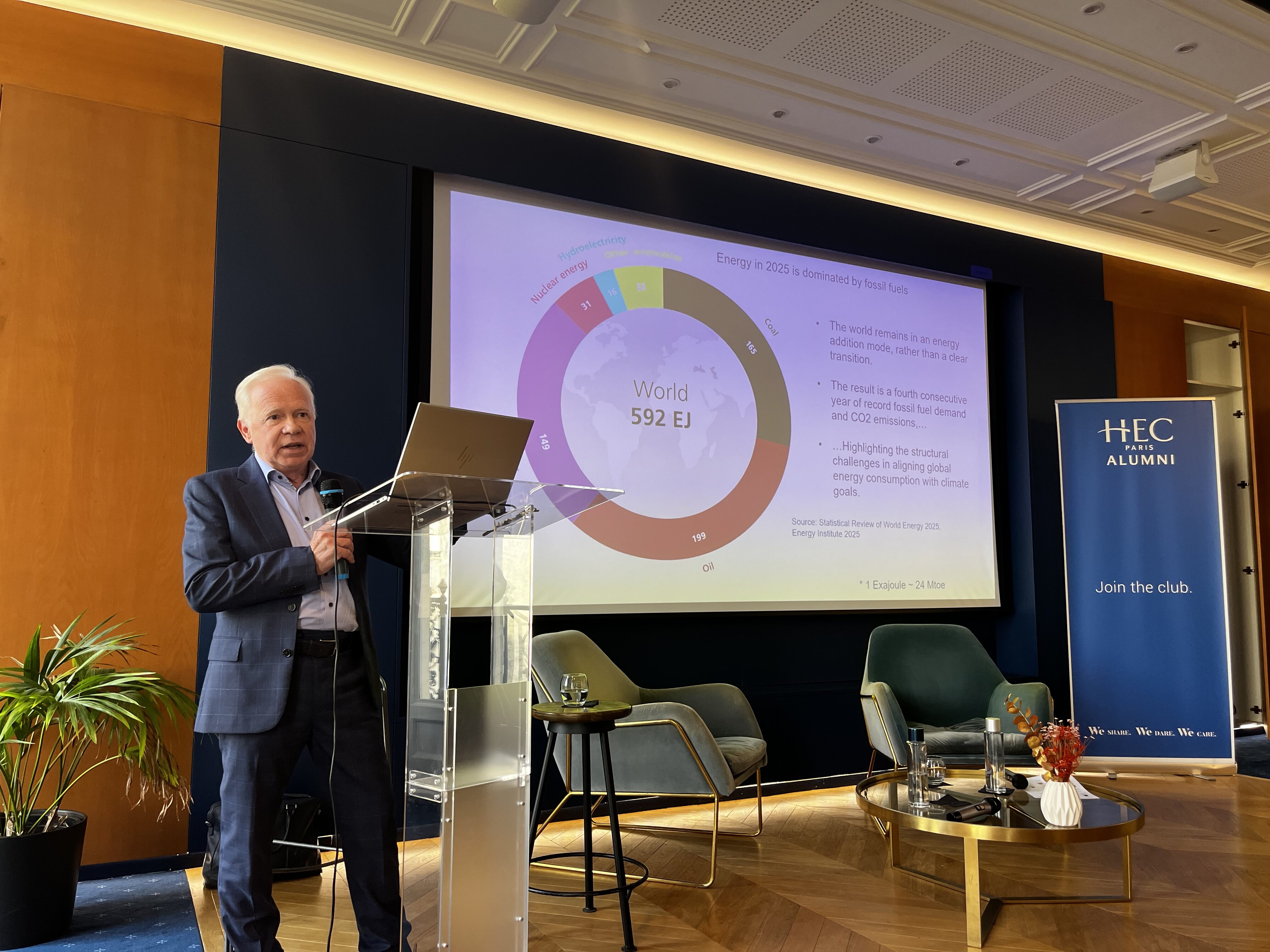

The fossil fuel economy is not behind us. It is still with us.

The first thing Jean-Michel established, with the precision of someone who has built financial models for oil majors and advised the European Commission and the French Ministry of Defence, is that the energy transition remains, for now, a far cry…

Today, more than 80% of global energy consumption is supplied by fossil fuels. That figure has not meaningfully changed in decades. The IEA’s Current Policy scenario — based not on ambition but on legislation already enacted, including the Paris Agreement as transposed into law by the EU27 — projects that in twenty-five years, the world will burn roughly the same volume of oil, gas, and coal as it does today. Not less. The same. And perhaps even more.

“We are in an addition mode, not a transition mode,” Gauthier said. “We assume energy demand will go up and up — and that means more coal, more oil, more gas.”

The cost of this trajectory, quietly accumulating in the atmosphere for over a century, is no longer abstract. CO₂ concentrations have never been higher. The 1.5°C target set by the Paris Agreement is, by the IEA’s own admission, no longer a credible projection. It is, at best, a normative aspiration.

The old geopolitics of energy: King Oil, and the dollar that priced it.

For those who lived through the oil shocks of the 1970s, the mechanics of today’s crisis feel familiar. The reason is structural and unresolved: 50% of proven global oil reserves sit in one region — the Middle East — with Saudi Arabia alone accounting for roughly 30% of that share. Gas tells an equally concentrated story: Iran and Qatar hold the bulk of Middle Eastern reserves; Russia and Turkmenistan dominate the CIS bloc. Four countries, in effect, hold the keys to the world’s conventional gas supply.

This concentration has imposed a singular risk architecture on the global economy for generations. And the entire edifice has been denominated in one currency: the US dollar, with prices set in New York.

“80% of the world’s energy supply,” Gauthier noted, “is extracted by one type of company — the extractive industry — all denominated in dollars, all ultimately held by pension funds.” That is the world we have lived in. It is also the world that is beginning to fracture.

The Strait of Hormuz: not the most dangerous chokepoint, but the most impactful for Asian economies.

The closure of the Strait of Hormuz, which precipitated this crisis, carries 25 million barrels per day of crude oil and petroleum products, almost exclusively destined for the largest Asian economies — China, Japan, South Korea, India. The bypass alternatives — the Ras Tanura–Yanbu pipeline at 5 million barrels per day, the Abu Dhabi pipeline to Fujairah at just over 2 million — offer a combined replacement capacity of 7 million barrels per day against a 25-million-barrel need.

“We are talking about the most severe energy shock ever,” Gauthier said. “At the time of the first oil shock in 1973, the shortfall was around 4 to 5 million barrels a day. Today, we are talking about 18 million barrels a day missing. Never mind 5. Never mind 2.” Add to that Qatar’s LNG exports — 77 million tons per year, the equivalent of 100% of Russia’s now-defunct gas contracts to the EU — and the scale of the disruption becomes clear.

Yet the Strait of Hormuz, Gauthier cautioned, is not the most dangerous waterway in the world. The Bab-el-Mandeb, controlled by Houthi rebels, carries 16% of global trade value. The Suez Canal — the artery through which Chinese clean energy technologies flow westward into Europe — carries more. The Strait of Malacca, in Malaysian, Indonesian, and Singaporean waters, handles 23% of international trade value and 24% of the global trade volumes. Should China’s military ever choose to act in that corridor, the consequences would dwarf anything the world is experiencing today. “The risk is way closer to home than we think,” Gauthier said. “Even the English Channel — 15% of global trade value — is a potential mega-risk for the global economy.”

The new geopolitics: from carbon to electrons, and from barrels to batteries.

Here is where Gauthier’s analysis becomes most consequential — and most uncomfortable for Western policymakers. The IEA’s net-zero emissions scenario by 2050 requires the world to move, in a single generation, from a system dominated by one molecule to one dominated by one carrier: electricity. Solar, wind, hydro, nuclear, advanced bioenergy — all converted into electrons. The transport sector, the steel industry, cement, petrochemicals — all electrified.

But electricity of that scale requires metals. Copper, lithium, cobalt, graphite, nickel, rare earth elements — neodymium, praseodymium, terbium, yttrium. And on nearly every critical mineral needed for the transition, current supply is dramatically short of the 2040 targets required to meet Paris Agreement commitments. “For lithium, we are very far off the mark,” Gauthier said. “For graphite — very far. The market for these materials will be terribly illiquid. Beware.”

More striking still is the geography of this new dependency. In the old world, the risk was concentrated in the Middle East, Russia, and the United States. In the new world, the risk map shifts to Central Africa — above all, the Democratic Republic of Congo, which Gauthier described “with a highly constrained access to capital and extremely weak institutions” — and to Central and South America.

And then there is China. Not as a miner of critical minerals — European, American, and Australian mining companies have better access to upstream reserves — but as the world’s dominant processor, transformer, and manufacturer. China holds up to 90% of the world’s processing and refining capacity for rare earth elements. It dominates solar PV manufacturing end-to-end. It dominates wind turbine production after which it simply absorbed the European leaders that had briefly emerged. It dominates battery cell production, electric vehicles, heat pumps. “The whole world may have access to copper and lithium,” Gauthier said. “But they have to go through China if they want the finished product.”

The price implication is structural: China has created massive excess capacity across all these technologies, which means the marginal cost of its excess plants sets the global price. Competing with that from Europe or North America is not a near-term possibility.

The transition’s deepest paradox: we subsidized demand, and created value elsewhere.

Asked about opportunities for companies willing to navigate this new landscape, Gauthier was characteristically direct: yes, the opportunities exist — but they will accrue, above all, to those operating under regulatory frameworks fundamentally different from the European Union’s. “When you look at the solar revolution in China, the wind revolution, the battery electric vehicle revolution — and you compare it to what we have done in Brussels — it is really night and day.” Europe subsidized demand. China subsidized technology and supply. The result: jobs, manufacturing capacity, and value creation in the East; market support costs in the West.

“We are still doing it,” he added, with a weariness that was not theatrical. “We are subsidizing demand instead of subsidizing technology and supply. Under any basic economics taught at HEC, that is the worst thing you can do.”

What the transition cannot avoid: the above-ground scarcity.

A question from the floor raised the ghost of peak oil theory — the 1950s geological thesis that we would eventually run out of oil. Gauthier dismissed it cleanly. “What we call reserves is a stock exchange concept, not a geological concept. Reserves are the barrels that can be extracted at today’s price. Under a high-price scenario, you have more reserves. The proved reserves of today are about 10% of the real geological recoverable base.”

The real scarcity, he argued, has changed sides entirely. “The scarcity is not below ground anymore. It is above ground. It is the inability of the atmosphere to absorb more CO₂. We are going to stop using oil whilst we still have billions of barrels in the ground — not because oil is missing, but because the atmosphere will not support more emissions. That is peak demand, not peak oil.”

The fracture is structural. The menu is clear.

Jean-Michel Gauthier ended his presentation by returning to the phrase with which he had opened it. We are not heading into a world of new risks, he said. We are heading into a world of new risks stacked on top of old ones. The long-standing vulnerabilities of the oil and gas system — Hormuz, Bab-el-Mandeb, the Middle East’s concentration of reserves — are not being replaced by the new world of critical minerals and clean technologies. They are being joined by them.

The vulnerabilities that produced this crisis remain unresolved: control over key transit routes is still contested, and the conditions for disruption remain in place. What the crisis has also revealed, as one observer noted in the Q&A, is that the energy transition is not an escape from geopolitical risk. It is a migration from one risk architecture to another — and the new one is, in some respects, more fragmented, less liquid, and harder to price than the one being left behind. On the evening of June 10th, this room had a better map than most.

“An evening as part of a dynamic that the club launched in 2025,” says Jérôme Bouquet (E.14), President of the HEC Alumni Energy Club. “In one year, we have organised six conferences — covering competitiveness, data centers, decarbonisation, energy networks, entrepreneurship, and tonight, geopolitics. The goal has always been the same: share high-level expertise, think collectively, and better understand the complexity of a sector that sits at the heart of our economies and societies.”

For Sarah Yarmohammadi (EM.19), bureau member and moderator of the evening, the ambition goes further: “Hosting this conference in English — a first for the club — and partnering with HEC UK to reach alumni beyond Paris, while welcoming a member of HEC Paris faculty, reflects exactly the kind of bridges we want to keep building.”

Conference organised by the HEC Alumni Energy Club and the Geostrategy Club. Speaker: Jean-Michel Gauthier, Affiliate Professor, HEC Paris (Finance — Energy & Finance). Conference moderation and synthesis by Sarah Yarmohammadi.

Published by La rédaction